History & Evolution of Disaster Risk Finance & Insurance

Over the past two decades, interest in financial protection has surged around the world, receiving greater attention from developing country governments, the private sector, donors, and international organizations. As a result, over the past decade, developing countries have started to catch up—and even get ahead—in developing and implementing public policy for financial protection, mostly through learning-by-doing and with support from international partners.

This path, however, has not been linear. Progress often took place in steps and spurts of activities as countries experimented with new tools and approaches. Advances in different areas of disaster risk financing have often taken place at the same time in different countries as governments were looking to address their unique challenges, from their own starting point. For example, some countries began by looking to develop strong domestic insurance markets to absorb disaster risk, while others focused on protecting their budget against disaster shocks or on increasing post-disaster liquidity.

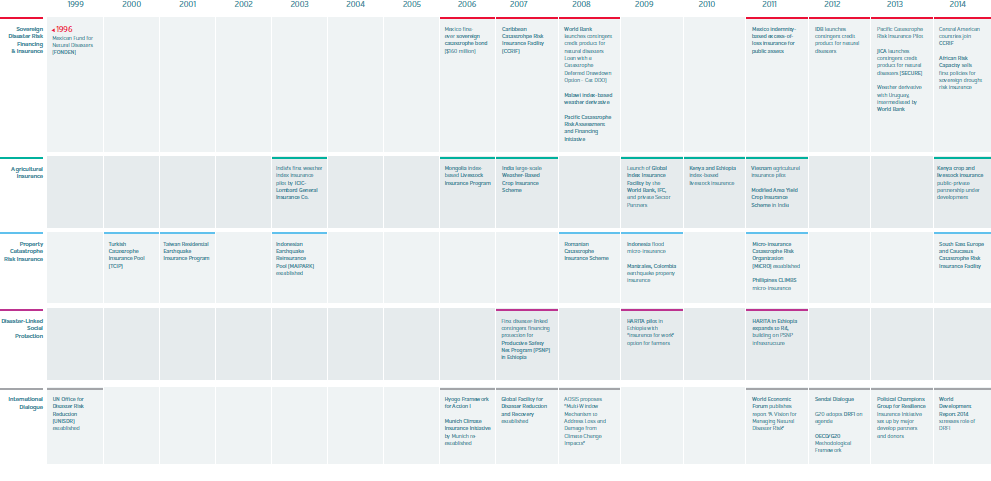

But patterns have emerged in the kinds of challenges that countries encountered while innovation has taken place in waves, pushing the boundaries of disaster risk financing and insurance. This section provides a broad overview of progress and evolution in disaster risk financing in developing countries since the beginning of the millennium, when an increasing awareness of proactive financial protection against devastating natural disasters had started to take hold. Too much has happened to capture here comprehensively, but key developments will highlight the lessons learned from this period (see Figure 10). Building on these lessons, this paper then presents an operational framework for financial protection.

At the beginning of the 21st century, most governments relied primarily on ad-hoc financing secured after an event to respond to natural disasters.

For most developing countries, especially, underdeveloped insurance markets, low technical and financial capacity of governments, and a longstanding culture in many countries of dealing with disasters mainly as a humanitarian issue meant that financial management of disasters remained mostly impromptu. Governments often relied on limited and uncertain means such as disaster funds, budget reallocation, and on donor assistance. The role of the ministry of finance was confined to approval of expenditures and identification and mobilization of funding sources after an event

Policy makers in developing countries began to recognize the benefits of proactive planning for the financial management of disasters. Early signs of success showed that setting up financial protection measures could help developing countries better manage the financial impact of natural disasters. The international community began to support financial protection measures before disasters hit and at the same time the 2005 Hyogo Framework for Action (HFA) went into effect, promoting more proactive disaster risk management.

New kinds of financial instruments to help address common problems in risk financing resulted in a string of market-based products for developing countries, including parametric catastrophe bonds and weather derivatives for national governments; disaster-dedicated contingent credit; and regional risk pooling mechanisms. Product innovation remained the focus until the end of the decade.

Increasingly, tailored financial products opened new opportunities for thinking about proactive financial protection in developing countries. Experiences, however, showed that stand-alone financial instruments are not silver bullets; they cannot solve all the challenges associated with the impact of disasters and must be integrated into a comprehensive disaster risk management strategy. A greater understanding of the need for more strategic risk management began to emerge towards the end of the decade. Efforts at better integrating the disaster risk financing and insurance agenda into the greater disaster risk management agenda was a turning point for the development of comprehensive financial protection against natural disasters in developing countries.

|

|

Regional risk pooling for Caribbean States |

|

| Providing contingent lines of credit for disaster risk financing |

By 2010, disaster risk financing and insurance practitioners had started working with a number of governments to design comprehensive disaster risk financing strategies rather than focusing on individual products (Mahul & Ghesquiere, 2010). Increasingly, the international community has recognized the disaster risk financing and insurance agenda’s importance in disaster risk management, public financial management, and financial sector development agendas. Increasingly, the use of financial decision making tools empowers governments to make more informed decisions. For example, financial decision tools can be used to evaluate potential fiscal risk caused by an earthquake risk transfer options to protect public debt portfolio. Or they allow governments to analyze the costs and benefits of different financial product and their potential impact on its medium-term budget. Experience suggests that sustainable, scaled up agricultural insurance should be based on an equal partnership between the public and private sectors. Ministries of finance have been increasingly taking the leadership in the development of disaster risk financing strategies, collaborating with other government entities such as disaster risk management agencies, insurance supervisors, and ministries of social welfare or agriculture. Additionally, the idea of a central government agency responsible for risk management has been proposed by international organizations and the private sector.

|

|

Strengthening subnational disaster risk financing capabilities |

|

| How risk modeling and analytics are informing disaster risk financing in Mexico |